Power transfer and policy dilemma, CD Markets interprets the changes in the Federal Reserve during the Warsh era

- 2026-05-21

- Posted by: CD Markets

- Category: financial news

On May 22, 2026, Kevin Warsh was officially sworn in as Chairman of the Federal Reserve at the White House, ushering in a new power cycle for the world's most important central bank. The CD Markets macro research team combines the latest personnel dynamics of the Federal Reserve, high-frequency inflation monitoring data, the long-term tracking system of the FOMC voting committee's position and changes in the global interest rate market to comprehensively dismantle the policy games and deep contradictions behind this handover, and help investors clarify the Fed's policy path and global market impact in the Warsh era.

Power transfer and inflation dilemma: The Federal Reserve enters a new stage of hawkish differentiation

The CD Markets research team pointed out that when Warsh took office as chairman of the Federal Reserve, the transfer of power and the rebound in inflation posed dual challenges. The Federal Reserve has entered a policy cycle dominated by hawks and intensified internal divisions. This handover breaks nearly 80 years of practice. Former Chairman Powell will stay on as a director until 2028 after his term ends to maintain the independence of the central bank. However, the "old and new under the same roof" pattern brings uncertainty to policy coordination. The Senate approved Warsh's nomination by a narrow margin, and the White House took charge of personnel arrangements throughout the process, highlighting the administration's intention to intervene in monetary policy. However, CD Markets believes that the differentiation of positions within the FOMC, institutional tradition and market inertia are the keys to truly constraining the direction of policy.

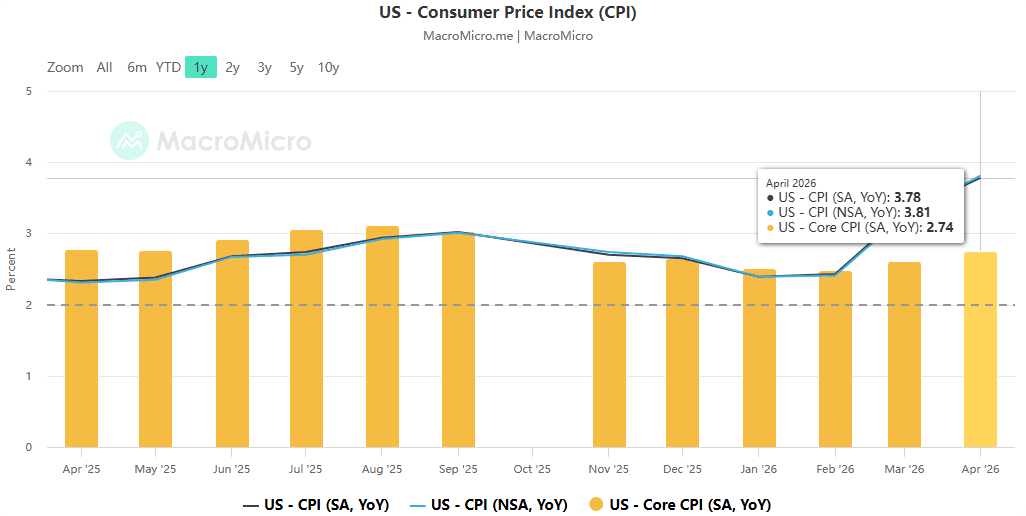

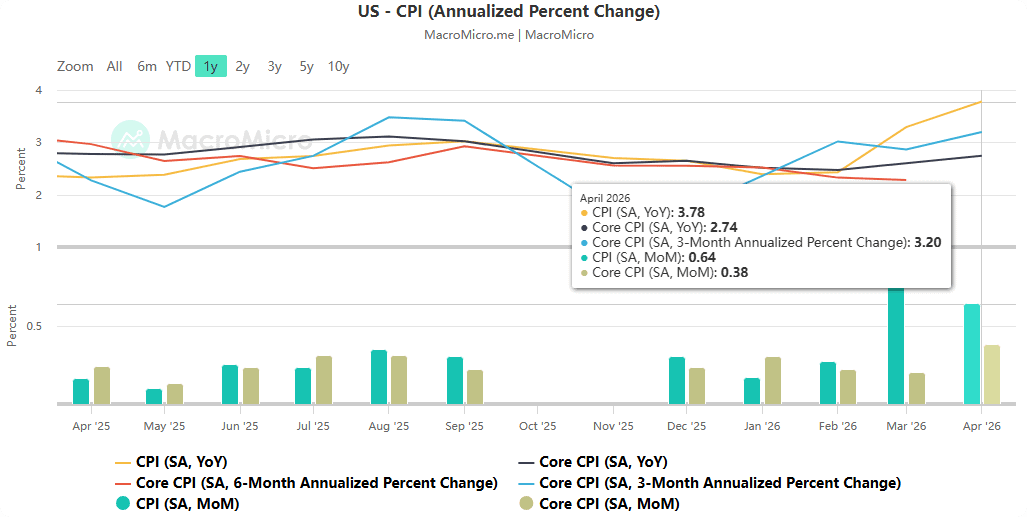

Warsh faced severe inflationary pressure upon taking office. Affected by the conflict between the United States and Iran that has pushed up energy prices, the U.S. CPI rose to 3.8% year-on-year in April, and the core CPI was 2.8%. Inflation in May is expected to exceed 4.18%, far away from the 2% target.油价暴涨带动全品类价格上行,通胀扩散趋势明显。 High inflation further intensified FOMC divergences. 4 月会议以 8:4 维持利率不变,4 票反对创 1992 年以来新高,鸽派要求降息、鹰派反对宽松表述。 The resilience of employment supports the hawkish stance. The Federal Reserve has turned hawkish as a whole, and market expectations have been rapidly revalued: the 2-year U.S. Treasury yield has risen sharply, expectations of an interest rate cut within the year have significantly cooled, and institutional bets on interest rate increases have increased significantly.

Wash Policy Framework: Three Core Pillars of Reputation Repair

As an "old acquaintance" of the Federal Reserve who served during the George W. Bush era, Warsh's policy propositions have formed a complete system. Through a comprehensive review of Warsh’s past public remarks, academic views and policy statements, and combined with the summary of Nick Timiraos, senior Federal Reserve reporter of the Wall Street Journal, CD Markets summarized its core policy logic as “repair of credibility and return to order”, which mainly includes three core pillars:

Inflation framework: Abandon tradition and evaluate inflation in real time

Warsh rejected the classic Phillips curve and attributed the main cause of inflation to excessive government spending rather than wage growth. He abandons the lagging traditional CPI statistical model and advocates dynamic monitoring of inflation through real-time commodity data. He believes that the Federal Reserve's adherence to inflation credibility can hedge against short-term energy inflation impacts.

Balance Sheet: Steady balance sheet reduction and strict compliance with policy boundaries

In response to the blurring of asset policy boundaries caused by the Fed's huge asset size of RMB 6.7 trillion, Warsh advocated re-clarification of policy boundaries, insisting on a gradual reduction of the balance sheet, resolutely rejecting radical adjustments, and preventing short-term and crude repairs of long-term accumulation of existing problems.

Communication mechanism: restrain speaking and focus on long-term order

Warsh abandoned the Fed's operating model of frequently predicting interest rates, and advocated reducing short-term market intervention and policy pronouncements, avoiding political risks, focusing policy on the stability of the long-term monetary order, and weakening short-term fine-tuning at a single meeting.

Triple reality constraints: Difficulties in implementing policy blueprints

The CD Markets policy deduction team believes that Wash’s ideal policy blueprint will face three insurmountable practical constraints, and its reform process is destined to be slow rather than disruptive:

- Mechanism constraints: Warsh has no authority to replace existing members of the FOMC, and the differences in the positions of the 18 voting members are difficult to quickly bridge. Many current officials have publicly defended current policy tools, and Powell's continued presence as a board member adds to the complexity of policy coordination. Former Philadelphia Fed President Harker said bluntly that Warsh is destined to fail to fulfill the executive's expectations for an interest rate cut - under the current inflation situation, there is no realistic basis for interest rate cuts.

- political constraints: The administration clearly requested a “significant interest rate cut” when nominating Warsh, but the hawk-led FOMC and the reality of high inflation make this goal almost impossible to achieve. Warsh must walk a tightrope between "administrative expectations" and "central bank independence" to balance the demands of both parties.

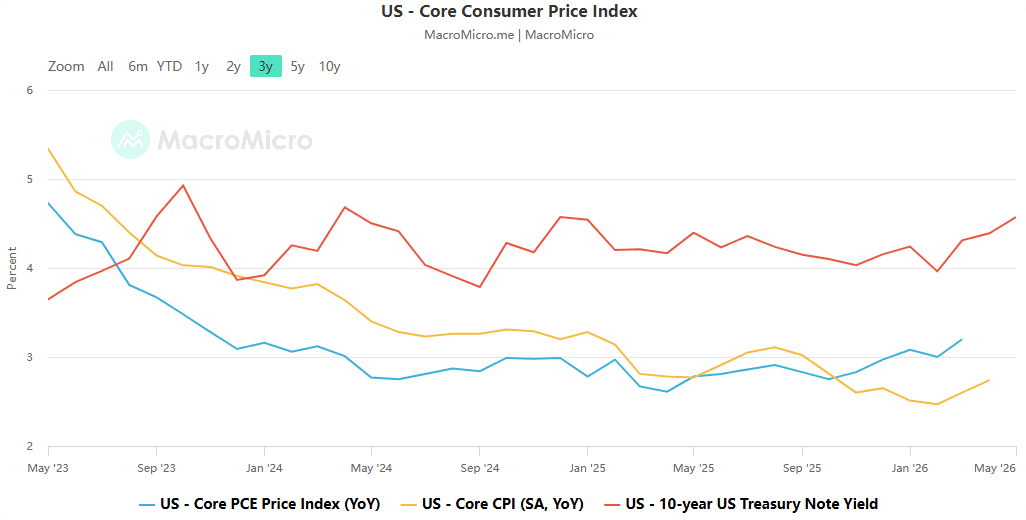

- environmental constraints: Warsh previously believed that “conditions for interest rate cuts are gradually being met.” However, the energy shock caused by the Iran conflict completely disrupted the original policy logic. Inflation soared from 2.4% to nearly 4%. The prerequisites for the application of the original policy framework no longer existed, and the space for policy balancing techniques was greatly compressed.

Preview of the first show in June: Signal changes in the pause

CD Markets' baseline forecast of the Fed's policy path shows that Warsh will keep interest rates unchanged at the first FOMC meeting hosted by June 16-17, and the window for rate cuts during the year has basically closed. The real highlight of this meeting is the adjustment in the wording of the policy statement - there is a high probability that the statement "retaining the tendency to cut interest rates in the future" will be deleted, sending a clear signal to the market that "anti-inflation is a priority". This is not a disruptive policy revolution but a careful framework calibration.

As Warsh has publicly stated before: "The Fed does not need revolution. What it needs is the restoration of credibility and the return of order." Under the triple pressure of rebounding inflation, internal divisions, and political games, every decision made by the new chairman will affect the nerves of the global market, and the May CPI data released on June 10 will become the first touchstone to test his policy determination. CD Markets judged that the Federal Reserve has officially entered a new stage of "hawkish dominance, intensified differences, and slow progress of reforms." We will continue to track the Fed's policy trends, changes in inflation data and global market linkages, and provide investors with the most cutting-edge policy interpretations and asset allocation guidance in a timely manner.