Will gold prices fall as geopolitical tensions cool? You may have mistaken the core logic of this round of gold

- 2026-05-26

- Posted by: CD Markets

- Category: financial news

The CD Markets global interest rate and precious metals research team is based on the self-built U.S. bond yield structure dismantling model, the central bank's gold purchase high-frequency tracking system and the cross-market asset pricing linkage framework, combined with the current global bond market, geopolitical situation and the latest developments in major asset classes to judge: Although the market is trading in expectations of cooling down conflicts in the Middle East, the core support of this round of global high-yield environment is not the short-term geo-premium, but three major structural factors: fiscal deficit expansion, AI capital expenditure wave and global savings investment balance reversal. Even if geopolitical risks completely subside and inflation falls in stages, it will be difficult for the global interest rate center to return to the low normal after the financial crisis. Gold is ushering in a new pricing cycle dominated by two sets of logics: "interest rate suppression" and "credit hedging."

Bond market drives logical differentiation: real interest rates become the short-term core suppression of gold

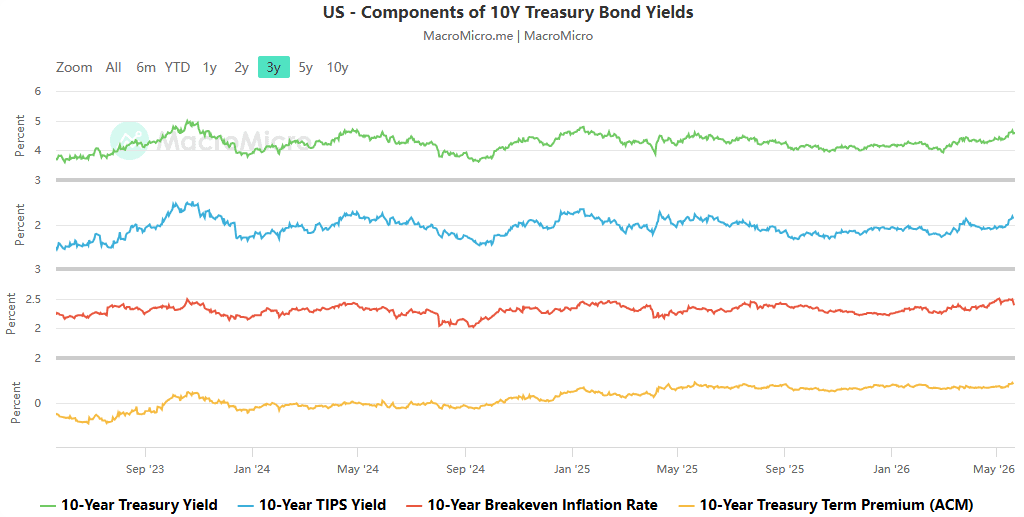

High-frequency market data tracked by CD Markets shows that the current trading logic of the bond market has significantly diverged: Although oil price fluctuations remain the short-term market focus, as of late May, the U.S. 10-year breakeven inflation rate remained at around 2.48%, about 50% lower than the peak of 3.0% in the first half of 2022. basis points, the upward trend clearly lags behind the nominal yield, indicating that the core driving force for this round of rising U.S. bond yields is real interest rates, rather than the "war inflation" expectations that the market had been generally worried about.

From the perspective of the global market structure, the driving factors for yields in different economies show clear differentiation: the current rise in yields in the United States is almost entirely driven by real interest rates, while the rise in long-term interest rates in Japan and Germany is dominated by inflation expectations. Under the traditional pricing framework, real interest rates are the core headwind factor for gold - the rise in real U.S. bond yields directly raises the opportunity cost of holding zero-coupon gold. This is also the core trading logic that has caused gold to fall into high fluctuations and periodic retracements since May as long-term U.S. debt sell-offs and interest rate hike expectations have revived.

The high interest rate environment is difficult to reverse: geopolitical cooling cannot resolve structural pressures

CD Markets emphasized that even if the geo-risk premium in the Middle East completely subsides, it does not mean that global long-term interest rates will fall significantly. After the market reported on May 25 that the United States and Iran were close to reaching a shipping stability framework in the Strait of Hormuz, crude oil, gold and other safe-haven assets simultaneously experienced short-term retreat. However, this fluctuation only came from the rapid dissipation of the geo-pulse premium and did not change the underlying support of the high-yield environment.

Through dismantling the micro-trading structure of the bond market, CD Markets found that the current market is re-pricing structural problems that cannot be solved through diplomatic statements or short-term ceasefires: the U.S. 10-year Treasury bond yield was close to 4.70% in May. Even if it subsequently fell back to around 4.56%, the core driver of its upward trend has always been the real interest rate, not the impact of a single event. This means that "high real interest rates remain at mid-to-high levels" is changing from a temporary cyclical state to a medium-term feature of market consensus.

The core paradox of gold pricing: the two-way tug-of-war between interest rate suppression and credit support

It is the structural root cause of the high-yield environment that forms the underlying support for gold not to be completely suppressed by high interest rates. CD Markets summarizes this as the core paradox of current gold pricing:

- Traditional suppression logic: High real interest rates raise the cost of gold holdings, and funds flow back to interest-paying U.S. debt assets, posing short-term headwinds for gold prices;

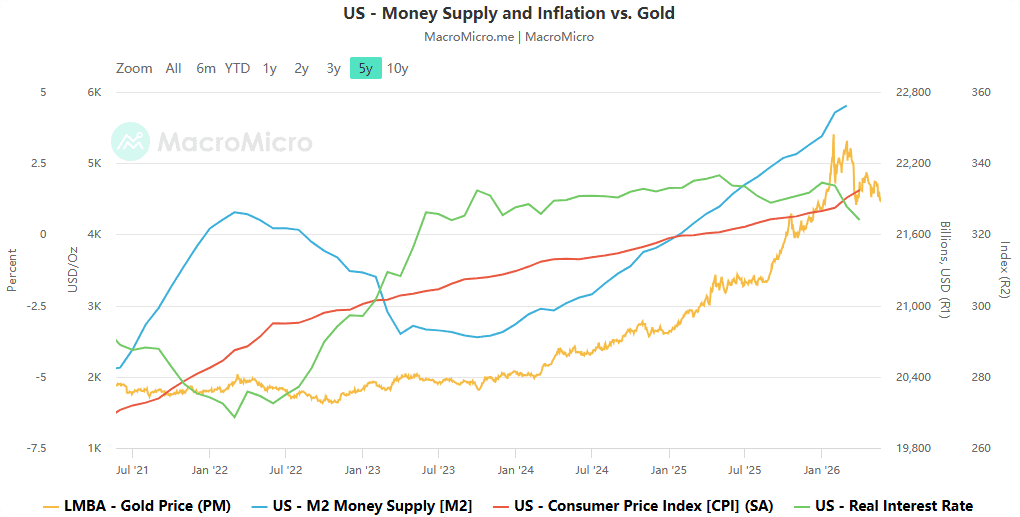

- Emerging supporting logic: The erosion of U.S. dollar credit caused by the long-term U.S. fiscal deficit and the spiral expansion of debt interest rates is re-pricing gold from a “non-interest-paying bond substitute” to a core asset for hedging sovereign credit tail risks, continuing to lift the bottom center of gold prices.

CD Markets' long-term calculation of the U.S. fiscal balance shows that the current scale of U.S. federal debt has exceeded $38 trillion, with annualized interest payments reaching $1.2 trillion, which has exceeded defense spending. The annual fiscal deficit remains at the level of $1.8 trillion. The negative spiral of "deficit expansion → increased debt issuance → rising interest rates → further expansion of the deficit" is being priced by the market as the long-term credit risk of U.S. dollar assets, rather than a purely cyclical problem. At the same time, global central banks have been net buying gold for 15 consecutive quarters, and structural buying with low price elasticity has further consolidated the bottom support for gold prices.

This is also the core reason why the explanatory power of real interest rates for gold has continued to decline in recent years - when the market begins to question "whether U.S. debt is still a risk-free asset," gold can maintain its strength in an environment where real interest rates are positive. The impact of the AI wave on gold also shows two-way characteristics: in the short term, the expansion of AI capital expenditures pushes up real interest rates and term premiums, indirectly suppressing gold prices; but in the medium term, the productivity improvements brought by AI may delay the outbreak of the fiscal crisis. At the same time, the concentration risk of the US stock AI track will also create a need for portfolio rebalancing, promoting the increase of funds in gold as a diversified asset.

Global interest rate differentiation and gold’s long and short cycle outlook

The CD Markets global macro monitoring system shows that the current upward path of global interest rates is significantly differentiated: Europe is affected by energy price fluctuations, Japan is superimposed on compensation demands for lagging central bank policies, and the UK is superimposed on fiscal expansion and political uncertainty. The actual upward rate of interest rates in non-U.S. economies is much weaker than that of the United States. This significantly alleviates the opportunity cost pressure on gold from the perspective of non-U.S. investors.

Based on comprehensive multi-dimensional model calculations, CD Markets makes the following judgment on the trend of gold:

- Short term (0-3 months): If the real interest rate of U.S. debt rises further and the geographical premium in the Middle East continues to retreat, gold prices will still face periodic correction pressure. The attractiveness of bond assets will increase under high real interest rates, and the traditional negative correlation pricing logic will return in stages;

- Midline (6-12 months): Structural factors such as the long-term U.S. fiscal deficit, the debt interest spiral, the continued erosion of U.S. dollar credit, and the global shortage of safe assets are building a higher bottom range for gold. The credit risks brought about by fiscal expansion are replacing simple interest rate cut expectations and becoming the core driver of gold's long-term trend.

CD Markets believes that the stronger the "structural" characteristics of this round of global high-yield environment, the more real the short-term headwinds for gold will be; but it is also the root cause of the high-yield environment - unfettered fiscal expansion and the irreversible expansion of sovereign debt, which form the underlying support for gold's long-term value. The next trend of gold prices is essentially the market answering a core question: whether U.S. debt is a "risk-free asset with temporary high interest rates" or a "high-risk liability with returns."